Venmo’s redesign signals a privacy pivot—yet stops short of true privacy-by-default

Venmo’s latest user-interface redesign is more than a cosmetic refresh; it is a strategic statement about what the platform wants to be in 2026: a social payments network where transactions are not only functional but also expressive. The most consequential change is also the simplest: new users now default to “friends only” transaction visibility rather than “public.” After years of criticism that Venmo’s public feed normalized oversharing of sensitive financial behavior, this adjustment acknowledges a growing market reality—privacy expectations have shifted from “nice to have” to baseline.

Yet the redesign also illustrates the difference between *privacy-aware* and *privacy-first*. Venmo’s new default reduces exposure for first-time users, but it does not fully resolve the structural risks that come from treating privacy as a setting rather than an architectural principle. Notably:

- Contact lists still default to public, preserving a discoverable social graph.

- The app still does not present “only me” as a default transaction posture.

- Privacy controls remain buried in menus, meaning the safest configuration requires proactive, informed user behavior.

In practice, this creates a two-tier reality: users who know where to look can harden their privacy, while less technical or less vigilant users remain exposed—precisely the population most vulnerable to harassment, profiling, or social engineering.

The social feed grows more expressive—while metadata risk quietly compounds

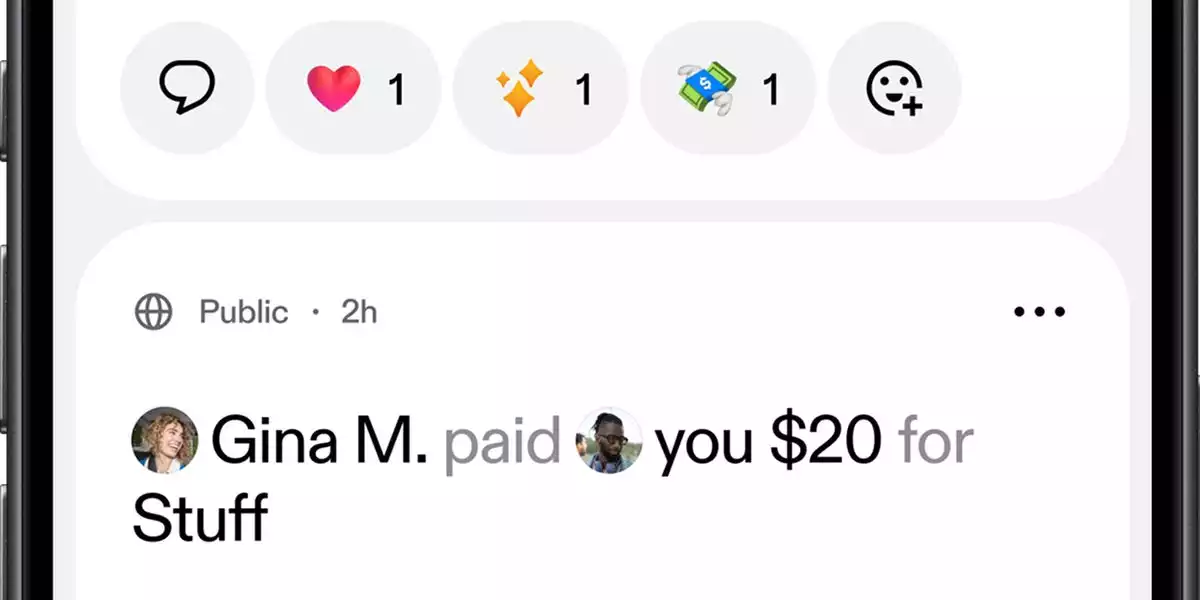

The redesign’s emphasis on larger images and animated GIFs underscores Venmo’s long-running differentiator: payments as social communication. From a product-growth perspective, this is coherent. Social features drive engagement, and engagement drives retention—especially in a category where the core utility (sending money) is increasingly commoditized.

But in fintech, every layer of expressiveness can also become a layer of risk. A richer social interface tends to generate richer metadata: who interacts with whom, how often, in what contexts, and with what linguistic or visual cues. Even when transaction amounts are not displayed, the combination of timing, counterparties, captions, emojis/GIFs, and network proximity can reveal patterns that are highly inferential—useful for personalization, but also attractive for adversaries.

This is where UI/UX trade-offs become governance questions. A design that nudges users toward sharing—while requiring effort to lock down visibility—can unintentionally amplify:

- Profiling and inference risks (habits, relationships, routines)

- Targeted scams and impersonation (leveraging social context and contacts)

- Unwanted disclosure (roommates, employers, partners, or stalkers triangulating behavior)

- Reputational harm (misinterpreted captions or visible associations)

The most persistent vulnerability is the contact graph. Leaving friend lists exposed preserves one of the most valuable assets in consumer fintech: a map of real-world relationships. That graph can be scraped, correlated with public records, and operationalized for everything from marketing to malicious doxxing. In an era where identity resolution is increasingly automated, a public contact network is not merely “social”—it is a high-fidelity dataset.

High-profile account discovery highlights an uncomfortable truth: defaults become policy

Venmo’s privacy debate is not theoretical. The public discovery of prominent figures’ Venmo accounts—most notably Joe Biden and Vice President J.D. Vance, identified through their contact networks—demonstrates how quickly “harmless” visibility settings can become a national headline. The lesson is straightforward: defaults function as de-facto policy, because most users never change them.

This is where comparisons to GDPR- and CCPA-influenced design norms become unavoidable. Across consumer technology, regulators and litigators increasingly treat “dark patterns” and buried controls as evidence that companies are not meaningfully prioritizing user protection. Fintech sits in an even more sensitive category because transaction data is inherently intimate—revealing health issues, political donations, family dynamics, and location-linked routines.

Venmo’s move to “friends only” for new users is a step, but it still leaves a gap between what users *assume* a payments app does and what the platform *actually* exposes by default. A privacy-by-default model would typically include:

- Private-by-default transactions (“only me”), with sharing as an explicit opt-in

- Private contact lists by default, especially for new accounts

- First-run privacy prompts that explain exposure in plain language

- Accessible privacy dashboards surfaced prominently, not buried in settings

The reputational risk is not limited to celebrities. The same mechanics that enable journalists or hobbyists to map a politician’s network can enable criminals to map a vulnerable person’s relationships—then exploit that context with precision phishing, coercion, or impersonation.

Trust is becoming the competitive moat in digital payments—and regulators are watching

Venmo’s redesign lands in a market where differentiation is shifting. As peer-to-peer payments become table stakes, the next competitive frontier is trust: privacy posture, transparency, and governance. Rivals such as Cash App and Zelle have increasingly emphasized quieter, less performative payment experiences—an appeal to users who want money movement to feel like infrastructure, not social media.

That matters economically. Venmo’s social layer has historically powered network effects, but network effects can weaken if users perceive that participation carries hidden exposure. The platform also faces a monetization balancing act:

- Social engagement features can support new revenue experiments (brand partnerships, commerce, or advertising-adjacent models).

- But perceived insecurity can suppress engagement, reduce retention, and increase churn—undercutting those very opportunities.

- A counter-path is emerging: monetizing trust, through premium privacy controls, enterprise-grade partnerships, or white-label offerings that treat privacy as a product feature rather than a compliance checkbox.

Regulatory headwinds add urgency. U.S. policymakers are intensifying scrutiny of fintech data practices, and future rules may effectively mandate what consumers already expect: privacy-first defaults, clearer consent, and stronger accountability for exposure pathways like contact graphs.

Venmo’s redesign suggests the company understands the direction of travel. The open question is whether it will complete the shift—from a platform that *allows* privacy to one that *enforces it by default*. In digital payments, where the product is ultimately confidence, the next iteration won’t be judged by how expressive the feed looks, but by how reliably the system protects the people using it.

By

By

By

By

By

By

By

By