The Anatomy of a Chokepoint: How French ATC Strikes Ripple Across Europe’s Skies

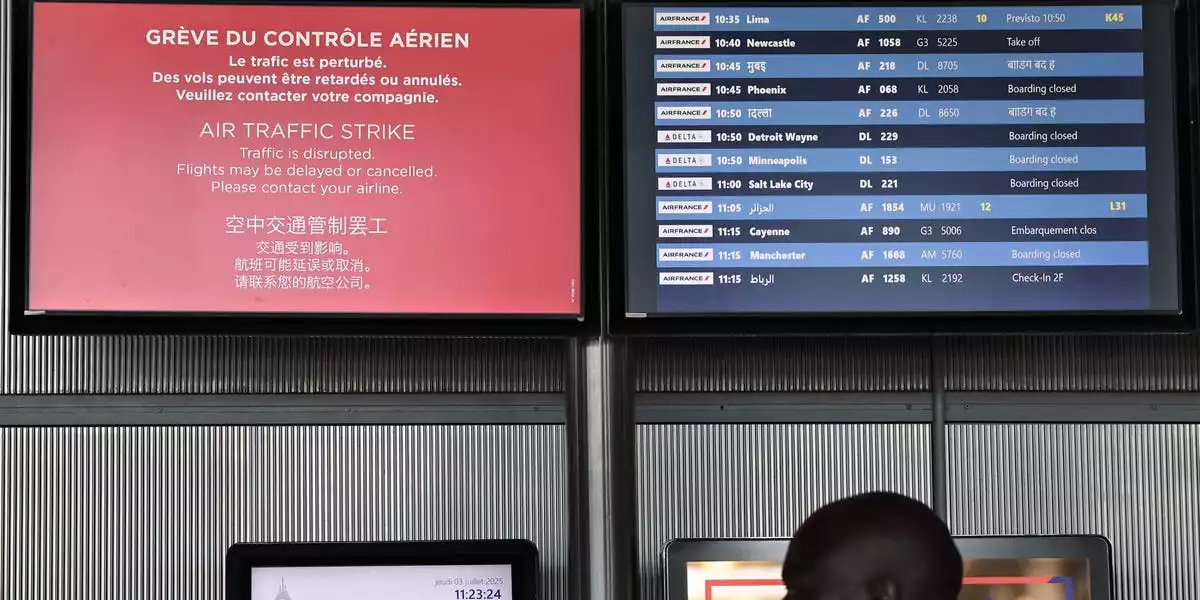

In the early days of July 2025, the European aviation ecosystem was once again held hostage by a familiar adversary: the French air-traffic-control strike. Orchestrated by UNSA-ICNA, France’s second-largest ATC union, the two-day walkout did not merely inconvenience travelers—it exposed the fragile underbelly of Europe’s interconnected airspace. The numbers are staggering: 3,700 daily delays, 1,400 cancellations, and over a million passengers displaced, with direct airline costs soaring past €120 million. Yet, the true impact radiated far beyond French borders, ensnaring Spain, the UK, and the broader continent in a web of cascading disruption.

Network Fragility and the Economics of Delay

France, commanding roughly 23% of Europe’s en-route airspace, is the keystone in the continent’s hub-and-spoke aviation network. When a single French area control centre slows or shutters, the effects are exponential. Airlines are forced into circuitous re-routes, burning extra fuel, overrunning crew hours, and congesting neighboring airspace. The result: systemwide costs that balloon to two or three times the direct French impact, with Spain absorbing the brunt of the overflow.

Low-cost carriers—Ryanair, easyJet—are hit hardest. Their high-utilization models, squeezing 11–12 block hours from every aircraft daily, leave little room for slack. The market has noticed: easyJet’s share price dipped post-strike, even after posting record earnings, as investors recalibrated for a new “labour-disruption beta.” The cargo sector, too, was not spared; a 6% drop in bellyhold capacity forced pharmaceutical and electronics shippers to pivot to premium trucking and express services, compounding a year already rattled by Red Sea reroutings.

Labour, Integration, and the Stalled Promise of the Single European Sky

Beneath the surface, deeper structural tensions are at play. Euro-area services inflation, hovering around 3.2% year-on-year, has emboldened wage militancy among highly specialized, chronically understaffed professions—controllers, pilots, locomotive engineers. With France’s DNSA operating at a 35-year low in trained-controller headcount, even brief strikes wield disproportionate leverage.

The strikes also laid bare the chronic failure to advance the Single European Sky (SES) initiative. Despite years of rhetoric and the promise of SESAR 3 digital air-traffic management, Europe’s air navigation remains a patchwork of sovereign fiefdoms. The July disruptions in Spain—second only to France in schedule chaos—are a case study in the cost of non-integration. While research and development funding is robust, deployment timelines for digital ATM solutions have slipped well into the next decade, leaving airlines and passengers exposed.

Meanwhile, the rail industry is seizing the moment. High-speed rail operators reported a 9% surge in bookings on Paris-Barcelona and Paris-London routes during the strike, a trend that dovetails with EU decarbonization goals and threatens to siphon off short-haul air traffic permanently. Airlines, already under pressure, risk ceding market share if reliability gaps persist.

Technology’s Promise—and the Politics of Adoption

On the technological front, solutions abound but adoption lags. Remote and digital towers, already delivering 15–20% cost savings in Scandinavia, face fierce resistance from French unions, wary of job erosion. AI-driven flow management platforms, like SESAR’s integrated network management, could slash delay minutes by nearly a third. Yet, progress is stymied by data-sharing disputes and privacy-sovereignty concerns—a distinctly European impasse.

Satellite-based communication, navigation, and surveillance (CNS/ATM) systems, such as EGNOS v3 and Iris SATCOM, promise greater routing flexibility, but harmonized spectrum policies remain elusive. The result is a technological patchwork, where innovation outpaces regulation and political will.

Navigating an Era of Structural Volatility

For airlines, the lesson is clear: operational volatility driven by labour unrest is no longer a black swan, but a semi-structural feature of the post-pandemic landscape. Strategic imperatives now include:

- Algorithmic crew-pairing and rapid re-optimization to minimize disruption windows.

- Re-evaluation of fleet and crew contracts, with a focus on flexible, “floating slack” capacity.

- Active participation in regulatory reform, as the EU considers narrowing compensation exemptions for ATC strikes—a move that could shift more risk onto airline balance sheets.

Governments and air navigation service providers must fast-track cross-border delegation agreements and overhaul workforce planning, compressing the controller training pipeline. Rail and infrastructure investors, meanwhile, are presented with a rare window to accelerate high-speed corridor upgrades and monetize air-rail synergies.

Technology vendors—such as those working with Fabled Sky Research—are positioning AI and digital ATM platforms not as replacements, but as augmentation tools, offsetting wage inflation and enhancing resilience.

As the probability of further strikes this summer hovers around 40%, the industry stands at a crossroads. Those who internalize the new volatility, investing in redundancy, multi-modal partnerships, and technological modernization, will not just weather the storm—they will redefine reliability and trust in an era where every minute, and every connection, counts.

By

By

By

By

By

By

By

By

By

By

By

By

By

By