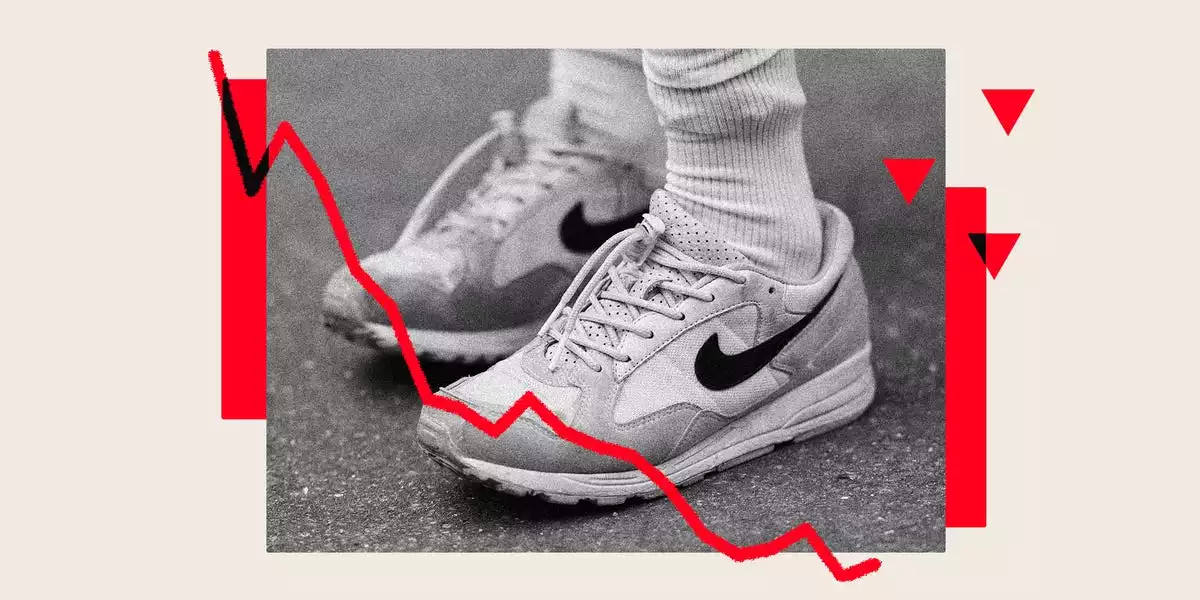

A storied brand meets a harsher market reality—and a more crowded performance landscape

Nike’s recent stock trajectory has become a proxy for a deeper strategic reckoning. With shares down roughly 70% from the November 2021 peak—and about 30% lower in 2024 alone—investors are no longer pricing Nike as an untouchable category-defining machine. They are pricing it as a global consumer brand navigating post-pandemic normalization, intensifying competition, and the aftereffects of a distribution strategy that prioritized efficiency over ecosystem strength.

The reinstatement of Elliott Hill as CEO in early 2024 signals a deliberate pivot: a “back-to-roots” reset that emphasizes core sports credibility, product innovation, and repaired wholesale relationships. That framing matters. Nike’s advantage historically has not been e-commerce mechanics or margin engineering; it has been the ability to translate elite sport into mass aspiration—then deliver it through a distribution network that amplifies the brand rather than merely transacts it.

Under former CEO John Donahoe (2020–2023), Nike leaned hard into direct-to-consumer (DTC), pulling back from major retailers. The move delivered near-term benefits—cleaner brand presentation, higher margins, tighter data capture—but it also weakened the “many storefronts, one narrative” model that made Nike ubiquitous. As challengers like Hoka and On gained mindshare, Nike’s reduced presence in key retail environments created whitespace competitors were eager to occupy.

The pandemic temporarily obscured these trade-offs. Demand surged, inventories moved, and scarcity dynamics were easier to maintain. As spending patterns normalized, Nike faced a more punishing reality: overstock, less “drop” magic, and a consumer willing to experiment with newer performance brands that feel fresh, technical, and culturally current.

—

The distribution pendulum swings back: rebuilding wholesale without abandoning DTC

Nike’s strategic recalibration is best understood as a search for equilibrium rather than reversal. DTC remains valuable for flagship storytelling, premium presentation, and customer data. But wholesale—especially in athletic footwear and apparel—still provides what DTC cannot replicate at scale: geographic reach, local merchandising expertise, and multi-brand discovery.

Hill’s approach implies a more pragmatic channel architecture built around three priorities:

- Re-onboarding and re-energizing key retail partners

Expect improved partner economics and tighter coordination on launches, allocations, and marketing. The goal is not simply to sell more units through wholesale, but to restore Nike’s presence where consumers browse, compare, and decide.

- Re-segmentation by sport to sharpen focus

A shift toward sport-specific “micro-businesses” (basketball, golf, trail, running) with clearer accountability can accelerate decision-making and reduce the one-size-fits-all product cadence that often dulls innovation.

- Channel synergy rather than channel rivalry

The most durable model is hybrid: DTC for narrative control and premium experiences; wholesale for scale, community presence, and the kind of curated scarcity that makes launches feel like events again.

This tension mirrors a broader pattern across industries. Legacy automakers, for instance, are discovering that pushing direct EV sales too aggressively can destabilize dealership networks that still drive service, financing, and local market penetration. Nike’s challenge is analogous: modernize distribution without breaking the ecosystem that helped build the brand.

—

Product and technology: why Nike’s turnaround is ultimately an innovation story

Nike’s renewed emphasis on “roots” is not nostalgia—it is a bet that performance leadership is the most defensible moat in a market where marketing alone no longer guarantees preference. The competitive set has evolved; challengers are credible, technically fluent, and fast.

Three technology and product implications stand out:

- Materials science as competitive re-acceleration

Reinvesting in proprietary cushioning systems, advanced knit constructions, and carbon-plate integration is essential to reclaim the perception that Nike sets the performance agenda. In running especially, the innovation gap has narrowed.

- Digital-physical convergence, not digital substitution

The next phase of Nike digital is less about steering consumers away from stores and more about embedding tools into the retail journey:

– augmented-reality fitting and guided sizing

– AI-driven personalization and recommendations

– in-store analytics that improve merchandising and sell-through

Done well, this turns wholesale partners into an extension of Nike’s digital intelligence rather than a separate channel with misaligned incentives.

- Supply-chain digitization as margin protection

Elevated inventory levels underscore the need for real-time demand sensing and AI-powered inventory optimization. The lesson of the past two years is blunt: forecasting errors are no longer just operational—they are brand-damaging, because heavy promotions erode prestige and train consumers to wait for markdowns.

A more ambitious possibility sits behind these moves: Nike could eventually platformize parts of its logistics and forecasting capabilities—monetizing internal expertise as a service for select non-competing partners. It’s not a near-term fix, but it reflects how leading firms increasingly convert operational excellence into new revenue lines.

—

Macro pressures and regional fault lines: the real test is execution over multiple quarters

Even with sharper strategy, Nike’s turnaround must contend with external constraints that complicate timing and outcomes:

- Tariffs and trade frictions continue to pressure gross margins, pushing sourcing diversification into Vietnam, India, and Latin America—often at higher unit costs.

- Greater China remains a pivotal swing factor. Nationalist consumption trends, strong local competitors, and uneven recovery beyond tier-1 cities make growth harder to “buy” with marketing alone.

- Inflation in labor and materials limits pricing flexibility, especially in lifestyle categories where differentiation is thinner and promotional intensity rises quickly.

Early 2024 signals suggest a tentative North American recovery, but Europe and China remain more challenging, and inventory is still elevated. Nike is not facing existential risk; it is facing a credibility test—whether it can restore momentum without sacrificing brand equity through excessive discounting or overcorrecting on channel strategy.

What happens next will be determined less by slogans than by operational discipline: cleaner assortments, fewer but better launches, tighter partner coordination, and innovation that feels unmistakably Nike. If Hill’s reset succeeds, it won’t look like a sudden rebound—it will look like a brand steadily reasserting performance authority, one product cycle and one retail relationship at a time.

By

By

By

By

By

By

By

By