Hospitality’s Fault Lines: When Platform Dependency Becomes Existential Risk

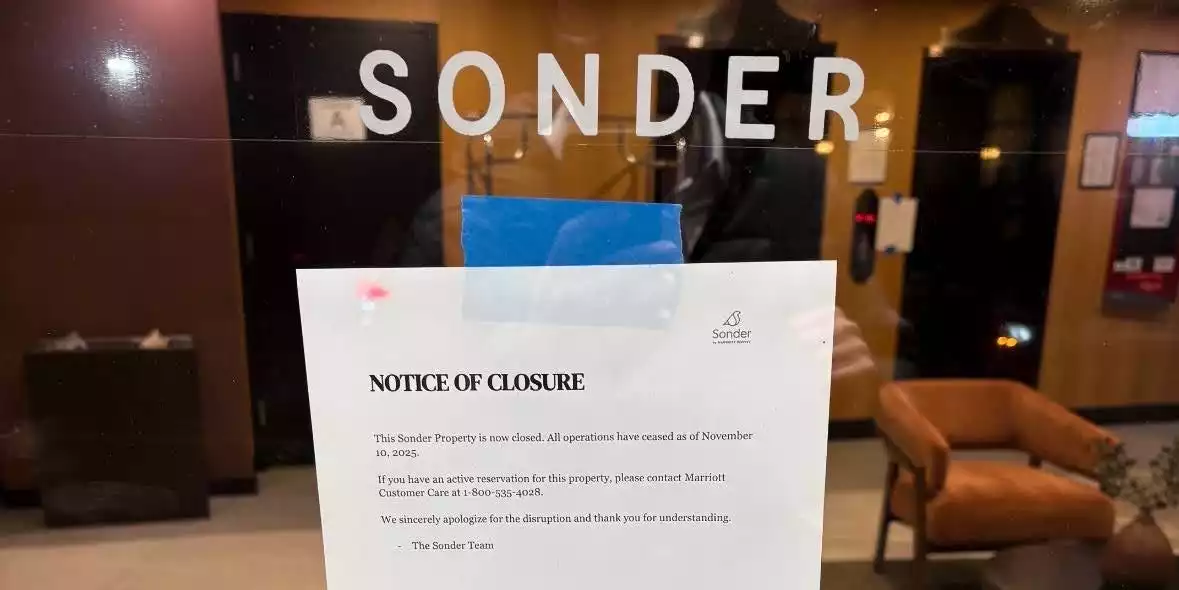

The hospitality sector, long a bellwether for platform innovation, found itself at the epicenter of volatility this week. Marriott’s abrupt termination of its white-label short-term rental partnership with Sonder—executed without transition buffers—triggered immediate guest evictions and operational chaos. Within days, Sonder filed for Chapter 11, a stark demonstration of how brittle the scaffolding of digital-era hospitality can be when a single enterprise gateway is yanked away.

Sonder’s collapse was not merely a casualty of misfortune, but rather a case study in structural dependency. Its technology layer—digital booking and operations atop leased real estate—was lauded for its efficiency, yet dangerously exposed to the whims of upstream channel partners. Marriott’s experiment with “Homes & Villas” was always about harvesting incremental demand without diluting brand equity; the split reveals a preference for asset-light affiliate models with rapid off-ramps, relegating partners to the precarious status of “vendor, not partner.” The lesson echoes Apple’s privacy pivot, which crippled ad-tech intermediaries overnight: in ecosystems where a single partner delivers more than 30% of volume, abrupt-exit scenarios are not theoretical—they are existential.

For executives, the imperative is clear: stress-test channel dependencies, map liquidity runways, and hardwire renegotiation triggers into contracts. Asset-light models do not immunize against liability-heavy realities, especially when the duration mismatch between multi-year leases and day-to-day bookings becomes unsustainable in a rising-rate environment.

Capital Markets: The Populist Rejection of Information Asymmetry

On Wall Street, the mood is no less febrile. Retail investors, emboldened by social media and battle-tested in meme-stock wars, continue to vilify short-sellers—save for the rare exception of Michael Burry, whose reputation for “truth discovery” distinguishes him from perceived manipulators. The populist distrust is less about market mechanics and more about a rejection of entrenched information asymmetry.

This sentiment is reshaping investor-relations playbooks. Radical transparency—live data rooms, real-time KPI dashboards—has become a defensive necessity, inoculating companies against the viral spread of short-squeeze narratives. The trust deficit is not easily bridged, but those who move first to demystify their operations may find themselves insulated from the next wave of retail-driven volatility.

Meanwhile, hedge funds are waging a talent war that presages broader wage inflation across knowledge industries. Multi-year “golden handcuffs” are replacing pure performance carry, as platforms seek to lock in alpha generators and reduce key-person risk. For technology and data leaders, this is a clarion call: revisit option-pool sizing, anticipate compensation inflation, and design retention packages that balance agility with loyalty.

The AI Compute Race and the New Economics of Autonomy

Tesla’s internal memo, signaling a relentless 12-to-18-month sprint to operationalize its AI stack—spanning Full Self-Driving, Optimus, and the Dojo supercomputer—underscores a tectonic shift in the economics of innovation. Labor intensity is giving way to model-training intensity; proprietary data exhaust is the new oil, and in-house compute the refinery.

The strategic calculus for boardrooms is shifting. Companies with durable data advantages—be it driving miles, fulfillment routes, or drone imagery—are accelerating capital expenditures on proprietary compute clusters. The “rent versus build” debate in AI infrastructure is no longer academic: those who control their own inference engines and data pipelines will enjoy lower long-run costs and greater data sovereignty. For others, now is the moment to negotiate multi-cloud burst pricing before GPU scarcity reignites.

Consumer Trust, Inflation Optics, and the New Social Contract

Beneath the macro headlines, a subtler drama is unfolding in the relationship between corporations and consumers. Even as headline CPI cools, essentials inflation—food-at-home, shelter services—remains stubbornly high, fueling political discord and eroding real wage gains. The risk for brands is acute: message discipline without tangible relief is discounted by consumers, especially in an age where social media delivers latency-free feedback.

To preserve brand equity, consumer-facing firms must pair pricing actions with visible value-add—loyalty bonuses, transparency in algorithmic decision-making, and even reversals of shrinkflation. Borrowing from open-source governance, publishing algorithmic accountability reports may soon become table stakes, pre-empting both regulatory scrutiny and social backlash.

Ultimately, the throughline connecting hospitality, capital markets, labor, and AI is the shifting locus of optionality. The winners will be those who institutionalize redundancy in distribution, liquidity in talent, and elasticity in compute—outpacing rivals still tethered to the comforting, but increasingly illusory, stability of legacy partnerships and cheap leverage.

By

By

By

By

By

By

By

By

By

By

By

By