A high-profile AI megacampus meets the hard physics of compute infrastructure

Fermi America’s appointment as “master developer” of the President Donald J. Trump Advanced Energy and Intelligence Campus was designed to signal scale, speed, and national ambition in the race for AI compute. Yet the company’s early trajectory—marked by cooling shortfalls, leadership departures, and a lack of commercial tenants—highlights a recurring truth in the data-center economy: branding and land do not substitute for engineering execution, bankable power, and pre-leased demand.

At the center of the story is Project Matador, a proposed 17-gigawatt AI data center campus in Texas that remains tenantless. The operational narrative has become more acute following the exits of CEO Toby Neugebauer and CFO Miles Everson, alongside reported internal acknowledgments of supply-chain miscalculations—particularly around cooling. With Fermi’s stock down roughly 71% over six months and a reported near-$500 million loss in 2025 against no consistent revenue, the project now reads less like a straightforward infrastructure build-out and more like a stress test of the AI data-center boom’s most aggressive assumptions.

For the broader market, the key issue is not whether AI demand is real—it is—but whether this specific form factor (a massive, single-site megacampus built ahead of committed tenants) can survive today’s capital markets, procurement realities, and tenant risk models.

—

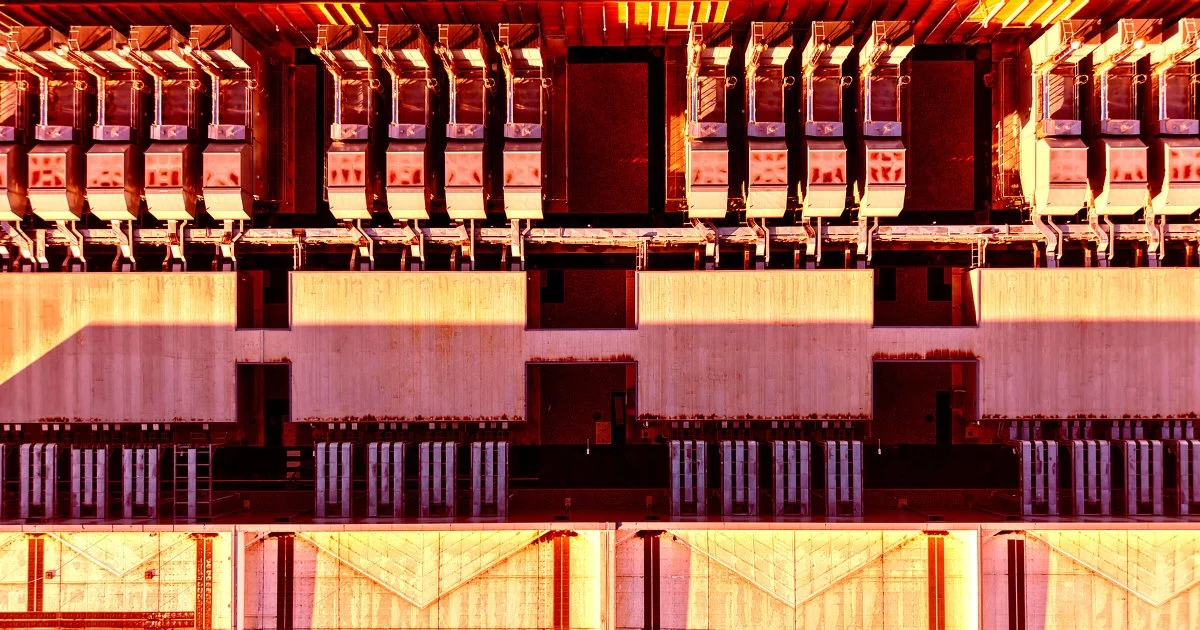

Cooling, power density, and procurement: where AI data centers succeed or fail

AI infrastructure is unforgiving because it is constrained by thermodynamics, electrical engineering, and supply-chain lead times. Modern AI clusters routinely operate at 30–60 kW per rack (and in many cases higher), pushing facilities toward liquid cooling or high-capacity chilled-water designs. That technical baseline changes the developer playbook: cooling is no longer a supporting system; it is a core product feature.

Fermi’s reported cooling-related missteps underscore several structural challenges that hyperscale and high-performance computing (HPC) operators evaluate early:

- Thermal engineering maturity: AI tenants increasingly expect proven reference architectures—cooling distribution, redundancy design, and validated performance under peak loads.

- Supply-chain orchestration: Chillers, heat exchangers, pumps, controls, and liquid-cooling components can carry long lead times. Misjudging procurement sequencing can stall commissioning even if the building shell is complete.

- Reliability and certification expectations: Enterprise and hyperscale buyers typically require Tier III/IV-like resiliency, plus third-party assurance (e.g., SSAE-18 controls reporting or Uptime Institute validation). Without credible pathways to certification, tenant conversations often slow or stop.

Just as important is the industry’s shift toward modular deployment. Prefabricated electrical rooms, containerized cooling, and phased capacity blocks allow operators to match capital outlay to contracted demand. Against that trend, a “megacampus first” approach concentrates risk: it increases time-to-revenue, amplifies construction and financing exposure, and makes the project more vulnerable to any single execution error.

—

Financing reality check: interest rates, Texas power volatility, and tenant risk calculus

The macroeconomic backdrop is materially different from the era when cheap capital could subsidize long-dated infrastructure bets. Higher interest rates and tighter credit conditions raise the bar for projects that are pre-revenue and capex-heavy. A near-$500 million annual loss, combined with the absence of contracted tenants, intensifies questions around refinancing risk, liquidity runway, and the feasibility of continuing development at scale.

Texas adds a second layer of complexity. The state can offer attractive economics and a deep energy ecosystem, but it also carries well-known exposure to weather-driven grid stress and price volatility. AI tenants—especially those deploying large training clusters—tend to prioritize:

- Long-term power purchase agreements (PPAs) with predictable pricing

- Firm capacity and interconnection certainty

- Operational continuity during grid events, often requiring on-site generation, storage, or robust curtailment strategies

Without secured PPAs and a credible energy-risk framework, even a well-located campus can struggle to convert interest into signed leases.

Then there is the reputational dimension. Associating the project with Donald Trump’s personal brand creates immediate visibility, but it can also introduce political and reputational risk for institutional investors and corporate tenants that prefer neutrality. In a sector where procurement decisions are often conservative and committee-driven, perceived controversy can become a friction cost—especially when paired with execution and financial uncertainty.

—

What Fermi’s predicament signals for the AI data-center market—and the viable paths forward

Fermi America’s situation is increasingly emblematic of a broader market sorting mechanism: the AI data-center boom is shifting from speculative land-and-power narratives to execution credibility—engineering depth, delivery track record, and contracted demand.

Several strategic pivots are commonly used to salvage or stabilize large, under-leased developments:

- Phased build-outs tied to pre-leasing milestones: committing in 25–50 MW tranches can reduce sunk costs and align capacity with real absorption.

- Partnerships with tier-one operators and integrators: joint ventures with established data-center builders, mechanical specialists, and power developers can de-risk cooling, commissioning, and PPA negotiations.

- Adaptive reuse and “data center as a service” (DCaaS): repositioning capacity toward predictable verticals—such as oil & gas HPC, climate modeling, or regulated enterprise workloads—may improve tenancy stability.

- Government and defense adjacency: domestic AI compute is increasingly framed as a national-security asset; structured engagement with federal procurement channels can provide more durable demand signals than purely speculative commercial leasing.

- On-site renewables and storage as a differentiator: integrating energy storage and renewable supply can hedge grid volatility and appeal to ESG-driven buyers, while also improving operational resilience.

The market is not rejecting AI infrastructure—it is rejecting unpriced risk. Projects that combine credible engineering, modular scalability, bankable power, and tenant-aligned delivery schedules will continue to attract capital and customers. Those that lead with scale before fundamentals may find that, in AI data centers, the most expensive mistake is building certainty after the fact.

By

By

By

By

By

By

By

By

By

By

By

By