A landmark U.S. public-market entry for humanoid robotics

Agility Robotics’ agreement to merge with Churchill Capital Corp XI, valuing the company at roughly $2.5 billion, is more than another SPAC headline—it is a signal that humanoid robotics is crossing from prototype theater into operational finance. The transaction is expected to deliver more than $600 million in gross proceeds, combining $420 million from Churchill XI with a $200 million Foxconn-led private placement, giving Agility the kind of balance-sheet runway that hardware-heavy AI companies typically struggle to secure in volatile capital markets.

What makes this deal unusually consequential is the commercial posture behind it. Agility’s humanoid robot, Digit, is already deployed across nine customer sites, including marquee industrial and logistics names such as Amazon and Toyota. The company also reports more than $300 million in multiyear orders for its next-generation Digit v5, a figure that—if it converts into delivered fleets and recurring services—could help shift investor perception of humanoids from speculative R&D to bankable automation infrastructure.

This is also being framed as the first U.S. IPO pathway centered on a humanoid-focused enterprise, arriving as global competitors accelerate: Tesla’s Optimus program continues to mature, Boston Dynamics pushes deeper into commercialization, and Chinese OEMs—reported to account for about 90% of last year’s humanoid shipments—are scaling deployments with manufacturing velocity that Western firms are still working to match. Against that backdrop, Agility’s public-market move reads as both a funding event and a strategic statement about where the U.S. intends to compete.

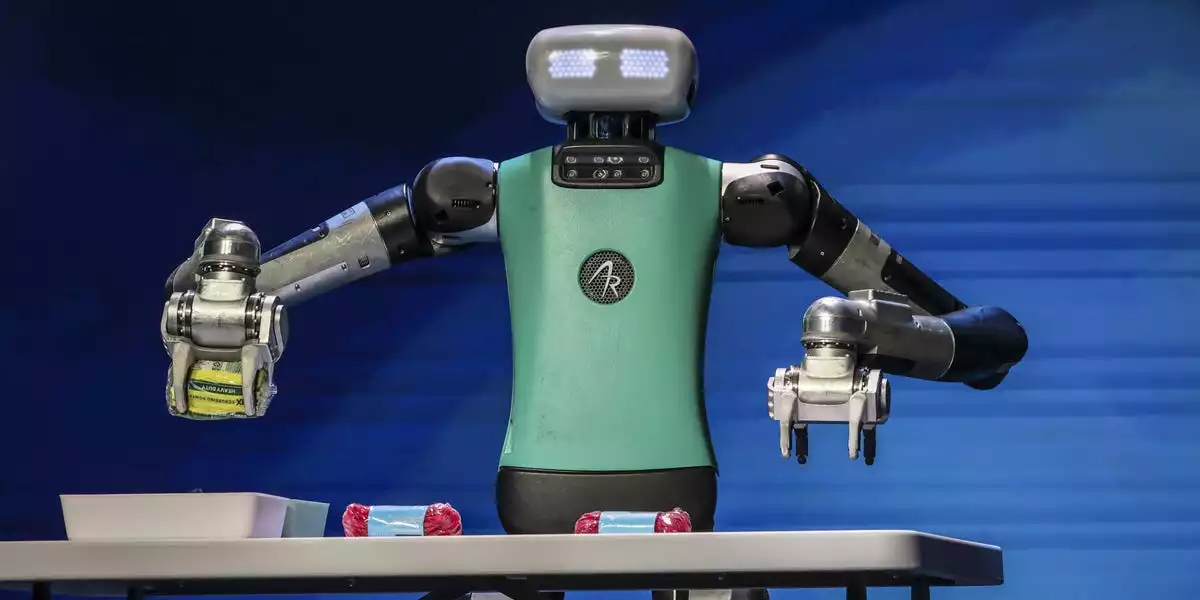

Digit v5 and the engineering pivot from demos to uptime

The most telling technical detail in the announcement is not the humanoid form factor—it is the explicit focus on industrial duty cycle. Digit v5 is described as having rapid-charge batteries engineered for 20-hour daily operation, a specification that aligns less with lab benchmarks and more with the rhythms of warehouses, retail backrooms, and light manufacturing lines where downtime is the true cost center.

That shift matters because the humanoid category has long been constrained by a familiar set of blockers: limited runtime, fragile autonomy in dynamic spaces, and safety models that require cages, barriers, or heavily structured environments. Agility’s roadmap suggests an attempt to tackle those constraints directly through a combined hardware-and-safety stack:

- Energy management as a product feature: A 20-hour operational target implies not only improved batteries but also tighter power budgeting across actuators, compute, and motion planning—critical for predictable shift-based deployment.

- Kinematics tuned for repeatable work: Better motion control is less about acrobatics and more about consistent handling of variable loads, floor conditions, and human proximity.

- Safety designed for co-working: Digit v5 is paired with Nvidia’s forthcoming Halos for Robotics safety system, positioned to enable human-robot collaboration without physical barriers.

The Halos angle is particularly strategic. In many industrial settings, the difference between a robot that is “impressive” and one that is “deployable” is whether it can operate in shared space without forcing a facility redesign. A “soft barrier” approach—multi-modal sensing plus edge AI inference that predicts and prevents collisions—could become a cornerstone capability for humanoids seeking broad adoption in brownfield environments.

The economics of a SPAC revival—and the competitive race for unit economics

SPAC activity has cooled from its peak, which makes this transaction a useful read on investor appetite: capital appears willing to re-engage when a company can point to real deployments, contracted demand, and a credible path to scaling production. For Agility, the SPAC route also offers a pragmatic advantage: humanoid robotics is capital-intensive, and the public-market narrative tends to reward companies that can fund manufacturing scale while continuing R&D.

Still, the competitive bar is rising quickly, and the market is unlikely to grant a premium for “humanoid” alone. Differentiation will increasingly hinge on unit economics and measurable customer ROI, including:

- OPEX reduction through labor substitution or augmentation in repetitive material-handling tasks

- Uptime gains and operational resilience during labor shortages or peak demand cycles

- Error reduction and safety compliance, especially in mixed human-machine workflows

- Modular upgrade paths, where software and hardware refreshes extend fleet life rather than forcing full replacement

Agility’s ecosystem of backers and partners—Amazon, Nvidia, SoftBank, and Foxconn—also reads as an industrialization strategy. Nvidia brings AI compute and safety tooling; Foxconn brings manufacturing scale and supply-chain discipline; Amazon provides a proving ground where logistics automation is measured in seconds and basis points. This combination supports a plausible move toward robotics-as-a-service (RaaS), where recurring revenue from fleet management, maintenance, and software updates can smooth the volatility of hardware margins.

Standards, geopolitics, and what enterprise leaders should watch next

As a first-mover U.S. humanoid listing, Agility gains a platform to influence how the category is defined—particularly around safety certification, interoperability, and operational standards. If humanoids are to work alongside people without cages, the industry will need clearer norms that connect real-world deployments to regulatory expectations, from workplace safety agencies to international standards bodies.

Foxconn’s participation also adds a geopolitical dimension. With China currently leading shipment volumes, a U.S.-listed humanoid company tied to Taiwan’s manufacturing powerhouse hints at a broader effort to build non-China scaling pathways for next-generation automation. For U.S. logistics and manufacturing operators navigating reshoring and near-shoring pressures, domestically anchored humanoid supply chains could become a strategic procurement criterion rather than a political talking point.

For executives evaluating humanoid deployments, the near-term questions are becoming more concrete and less futuristic:

- Can the vendor demonstrate repeatable uptime and serviceability at scale?

- Does the roadmap integrate with existing WMS/MES systems and enterprise security requirements?

- Is safety engineered as a certifiable system, not a demo feature?

- What is the plan for training, supervision, and change management as robots enter human workflows?

Agility’s SPAC move crystallizes a broader transition: humanoid robots are being priced, funded, and evaluated as productive assets. The next phase will not be won by the most viral demo, but by the companies that can deliver fleets that work long hours, integrate cleanly into operations, and earn their place on the balance sheet.

By

By

By

By

By

By

By

By

By

By

By

By

By

By