A summer schedule shock exposes aviation’s core vulnerability: energy-price volatility

Between June 1 and September 30, airlines worldwide removed a striking amount of capacity from the market—more than 75,000 flights canceled and over 9.3 million seats eliminated—as jet fuel prices surged above $200 per barrel amid heightened geopolitical tension centered on Iran. The scale is notable not only for its operational disruption, but for what it reveals about modern airline economics: despite sophisticated revenue management and global networks, fuel remains the industry’s most unforgiving swing factor.

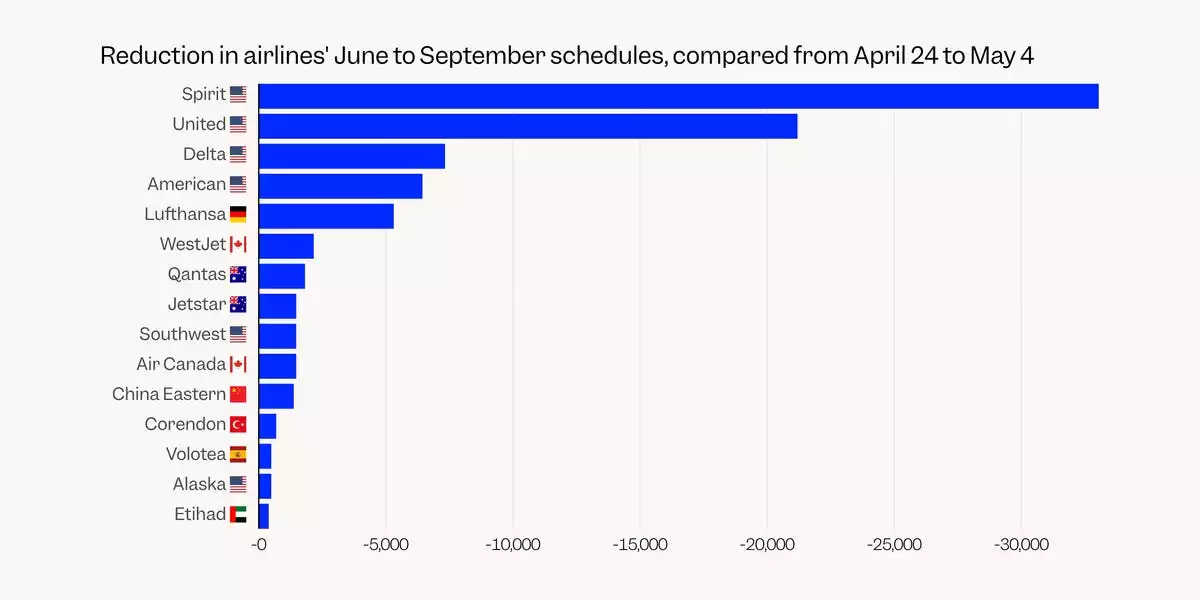

The distribution of cancellations underscores how quickly a fuel shock can become a competitive sorting mechanism. U.S. carriers led the pullback, with Spirit Airlines cutting roughly 33,000 flights before suspending operations entirely. Major network airlines also retrenched—United (~21,000), Delta (~7,300), and American (~6,400)—while Europe’s response was equally telling: Lufthansa canceled more than 25,000 short-haul departures, signaling that even diversified groups with dense hubs and strong corporate demand are not insulated when energy costs spike.

Yet the most revealing counterpoint came from Frontier Airlines, which moved in the opposite direction—adding more than 14,600 summer flights and opening new routes to capture displaced demand. In a market suddenly short of seats, capacity becomes both a pricing lever and a strategic weapon, rewarding carriers that can tolerate volatility longer—or manage it better.

Why jet fuel is forcing hard decisions faster than airlines can absorb them

Airlines can adjust fares, shift aircraft, and renegotiate some supplier contracts—but they cannot easily outrun fuel. When jet fuel rises sharply, the impact is immediate and nonlinear: margins compress, cash burn accelerates, and network plans built months in advance become obsolete. United’s reported $340 million first-quarter increase in fuel expense illustrates how quickly the cost base can move against even the largest operators.

Several structural realities intensify the pressure:

- Fuel is the largest variable cost after labor, and unlike labor it can reprice in days, not quarters.

- Fixed obligations don’t shrink with the schedule: aircraft leases, maintenance reserves, airport slot commitments, and labor agreements remain, even as flights disappear.

- Capacity cuts can protect liquidity but damage network integrity, weakening connectivity and reducing the value of hub-and-spoke systems that depend on frequency and breadth.

A key differentiator in this episode is fuel hedging strategy. Many European airlines have historically used more active hedging programs, while most U.S. carriers entered the summer largely unhedged, leaving them exposed to spot-market spikes. That strategic posture can be rational in stable markets—hedging can be costly and politically fraught when it backfires—but in a shock environment it becomes a magnifier. The result is faster retrenchment, and in Spirit’s case, a stark demonstration of what happens when a carrier with thin margins meets a sustained cost surge.

The technology and finance pivot: from static planning to real-time risk management

This disruption is also a referendum on airline decision-making systems. Traditional seasonal planning assumes relative stability in fuel and demand; today’s environment demands continuous recalibration. Airlines are increasingly piloting AI-enabled capacity planning and decision-support tools that ingest:

- fuel price indices and forward curves

- demand elasticity and competitive fare signals

- route-level profitability under multiple fuel scenarios

- operational constraints (crew, maintenance, slots, aircraft rotations)

The goal is not simply “better forecasting,” but faster, defensible decisions—when to cut frequency, when to upgauge aircraft, when to exit marginal routes, and when to opportunistically enter markets vacated by others.

At the same time, the fuel shock is reviving strategic interest in Sustainable Aviation Fuel (SAF) and longer-horizon propulsion research, including hydrogen. While SAF is not an immediate cost cure—supply remains limited and pricing often carries a premium—this moment strengthens the business case for airlines that can secure SAF blending partnerships, co-invest in supply, or negotiate long-term offtake agreements. The logic is increasingly twofold: cost resilience and regulatory alignment as emissions rules tighten.

Financial engineering is also evolving beyond plain-vanilla hedges. Carriers and financiers are exploring:

- structured commodity derivatives tailored to route networks and consumption profiles

- fuel-linked bond structures that share risk with capital markets

- consortium purchasing to pool negotiating power and smooth supply shocks

These approaches aim to reduce earnings volatility without creating balance-sheet distortions—an especially important constraint as interest rates rise and lenders demand tighter covenants.

Competitive realignment: low-cost agility, legacy network dilemmas, and the geopolitics premium

Frontier’s expansion amid widespread cuts highlights a broader market truth: flexibility is becoming a competitive moat. Low-cost carriers with simpler fleets, lower unit costs, and faster scheduling agility can move into gaps left by retrenching rivals—capturing both leisure demand and secondary-city traffic that becomes underserved when networks contract.

For legacy carriers, the dilemma is sharper. Deep cuts preserve cash, but they can also:

- cede strategically valuable routes to competitors

- weaken loyalty economics by reducing frequency and connectivity

- undermine premium revenue if corporate travelers perceive instability

This is where dynamic pricing engines and route-level profit modeling become central. The winners will be those that can reconcile yield management with disciplined capacity—protecting high-value corridors while trimming structurally unprofitable flying under extreme fuel assumptions.

Overhanging all of this is the geopolitical risk premium now embedded in energy markets. Tensions linked to Iran have introduced non-linear uncertainty across shipping routes, refining capacity, and supply expectations—forcing airlines to treat geopolitics not as an external headline, but as an input to network design and capital planning. Meanwhile, elevated fares collide with broader inflation, testing consumer discretionary spending and pushing airlines, hotels, and travel partners toward more creative bundling and pricing strategies to sustain load factors.

Spirit’s failed bailout effort also signals a tougher policy climate. If future public support emerges, regulators may attach conditions—resilience requirements, emissions targets, or hedging expectations—that reshape competitive dynamics long after fuel prices normalize. In this cycle, the airlines that endure won’t merely be those that cut fastest, but those that build operating models capable of flying profitably when energy, capital, and geopolitics all turn hostile at once.

By

By

By

By

By

By

By

By

By

By

By

By

By

By